By Alison Stafford, CFP®

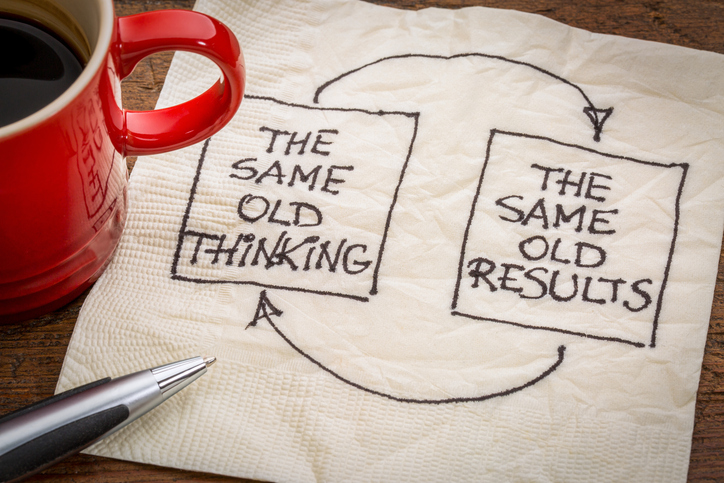

How often have you thought—I could get out of debt and save more for retirement, if only I made more money. It appears to make sense; that more money would be the answer to your financial worries. So it may surprise you, that debt often increases with higher income levels.

Stats Canada reported that households earning at least $100,000 had an average debt of $172,400. Compare that to households earning between $50,000 and $100,000, which had an average debt of $95,400. More income, more debt.

More recent data shows that in the second quarter of 2020, household credit market debt as a proportion of household disposable income fell from 175.4% to 158.2%, as household disposable income increased 10.8% and the stock of credit market debt remained relatively unchanged. In other words, there was $1.58 in credit market debt for every dollar of household disposable income.

If your first reaction to that is despair, you need to think about it in a different way. If you earn over $100,000 a year and still find yourself in debt, the challenge isn’t income, it is a mindset. And that puts you in the driver’s seat of change, so that is a good thing. Getting out of debt, saving for a home, or funding your retirement, don’t have to be dreams. They can be practical, achievable goals if you are willing to let go of some common money misconceptions.

We’ve identified the top five beliefs that sabotage high earners and offer new ways of looking at your spending and saving habits.

Misconception 1. Debt Is The New Normal

The fact that Canadians are in debt is not news. And when something is commonplace you stop thinking about it. You start believing it’s just the way things are. You may feel uneasy when you get your credit card statements, maybe you toss and turn some nights; but you allow yourself to feel better when you remember that most of your friends are in debt too. If everybody has the same problem, it must be normal, right?

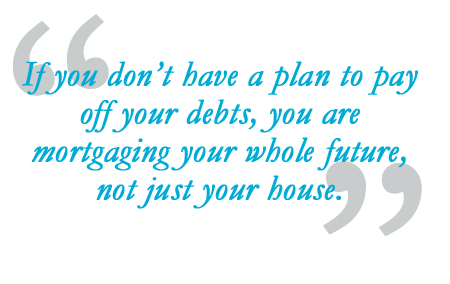

Not right at all. There is a price to pay. If you don’t have a plan to pay off your debt, you are mortgaging your whole future, not just your house. High earners assume they will be able to pay off their debts, so they are more likely to incur them without considering the consequences.

Not right at all. There is a price to pay. If you don’t have a plan to pay off your debt, you are mortgaging your whole future, not just your house. High earners assume they will be able to pay off their debts, so they are more likely to incur them without considering the consequences.

If you have $15,000 of credit card debt at 19% annual interest rate (APR), and you pay $500 each month, it will take you just over 3 ½ years to pay off. And you will incur over $5,500 dollars in interest. If instead of that monthly $500, you are paying only the required minimum, you will be paying years longer and will have paid interest equal to the price of a nice, new car.

That example was for a $15,000 debt, but the average high earner’s household debt is often 10 times that amount. Take a moment for that to sink in, and I think you will be willing to adopt a new view of debt.

New Belief: Financial freedom and peace of mind are possible when consumer debt is eliminated

Change your mindset about debt, before you even finish reading this post. Take an honest look at your debt and face the truth. Debt, in the form of a mortgage, has its place in a solid financial plan, but making ends meet through credit cards or credit lines, does not. Seize every opportunity to eliminate your debts, especially those with high interest rates, as quickly as possible. A financial professional can help you create an action plan.

Misconception 2. We Have Different Needs Than Past Generations

We have so much access to “stuff” that we have come to believe we need it. But the meaning of need hasn’t changed, it still means a necessity, a requirement, something essential. So we need to eat, but we don’t need to eat in restaurants several nights a week. We need shoes, but at what price and how many pairs? We need a roof over our head, but do we need exotic hardwood flooring under our feet?

You could argue that our generation does have new needs; perhaps in our world, access to the internet is a need, but does it need to be through the latest and greatest MacBook Pro? Or the newest smartphone?

The line between wants and needs has been blurred by a culture of consumption. If you are a high earner, with high earning friends, it can begin to seem that expensive clothes, cars, and travel are needs and not luxuries. The belief that you need to live a certain lifestyle, is a big factor in keeping high earners from getting ahead.

New Belief: Luxury and convenience are not needs

Don’t get me wrong. If you want, and can afford, any of these luxuries without going into debt, then by all means enjoy the fruits of your hard work. But do not compromise your future to keep up with the Joneses or to satisfy an inner child hooked on immediate gratification.

Don’t get me wrong. If you want, and can afford, any of these luxuries without going into debt, then by all means enjoy the fruits of your hard work. But do not compromise your future to keep up with the Joneses or to satisfy an inner child hooked on immediate gratification.

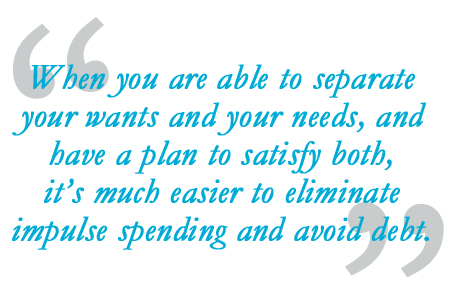

Get clear on what you really do need, now and for your future. Then prioritize your wants and save for those that matter most to you. When you are able to separate your wants and your needs, and have a plan to satisfy both, it’s much easier to eliminate impulse spending and avoid debt.

Misconception 3. A Money Management System is complicated and takes too much time

There are so many ways to pay for things these days, that we rarely touch actual currency. We type a credit card number online, we tap, insert, or swipe at stores, we have autopayments taken from our bank accounts and our credit cards. We can even pay for things through our phones and our watches. Which money is ours and which money is credit, doesn’t really register: it’s all just one big electronic portal to funds. Money flows in and money flows out.

Keeping on top of it all seems like a lot of work, so most people don’t. And denial has its charms if you are enjoying this flow of money. But most people will eventually have an inkling, deep inside, that they are losing control of it all. Those who ignore that twinge eventually hear from creditors, or discover that they won’t be able to retire when or how they imagined.

A Money Management System is well worth the effort. A system we’ve perfected at Money Coaches Canada.

New Belief: Successful people are engaged with their spending and saving

If you are struggling to get ahead, knowing how much you are spending and where you are spending it, is vital to turning your situation around. To improve your financial well-being, you must spend less than you earn; a task made easier when you are fully engaged with your cash flow.

Managing your money is empowering. It builds confidence and clears the spending fog. There are some great tools like Mint.com that can help you get organized. Money Coaches Canada has developed an On Track Money Management System that we introduce to all our clients. When money management becomes a habit, you will be far less likely to spend impulsively.

Misconception 4. I work hard, I deserve the nice things everyone else has

We live in a very voyeuristic world. Facebook and Instagram are filled with photos of people’s vacations, renovations, new cars, shopping sprees, parties, and more. Social media can warp our definition of success, by creating false measures of achievement.

In reality, many of the smiling people on social media are struggling offline, or worse, they are oblivious to the financial house of cards they are building. You work hard and deserve better than that. But some of those smiling folks are managing their money and making trade-offs based on their priorities. Maybe they choose to be a one-car family that eats healthy meals at home so that they can invest and save and take that fabulous trip to Rome on their Facebook page. That is something you do deserve: a financial plan that gives you choices and allows you to focus your money on things you value.

In reality, many of the smiling people on social media are struggling offline, or worse, they are oblivious to the financial house of cards they are building. You work hard and deserve better than that. But some of those smiling folks are managing their money and making trade-offs based on their priorities. Maybe they choose to be a one-car family that eats healthy meals at home so that they can invest and save and take that fabulous trip to Rome on their Facebook page. That is something you do deserve: a financial plan that gives you choices and allows you to focus your money on things you value.

New Belief: Financially successful people have priorities and are willing to make trade-offs

Don’t get caught up in comparing your lifestyle, with the lifestyles of your friends and co-workers. Few people can have everything they want, but with planning and priorities, you can achieve your goals. When you define what is important to you, giving up less important things, no longer feels like a trade-off—it’s just good sense.

Misconception 5. Life has too many variables, it’s impossible to stick to a financial plan

Many people associate a financial plan with rigid budgeting and want nothing to do with it. They believe that planning is about allotting money into categories and not spending a penny more than the number on the spreadsheet. Except that something always comes up, the numbers don’t work, and they feel lousy about their inability to stay on track.

Others mistakenly assume, that planning is all about investing and retirement funding, and they believe they are either too young, too old, not wealthy enough, or too in debt to have any money to spare for that sort of plan.

All those people are mistaken.

New Belief: A financial plan is a roadmap, not a rule book

Your life is a journey with lots of side trips, and your money is the fuel that gets you where you’re going. But if you head off without a map, you’ll waste, or even run out of fuel, before you get where you’re headed.

Your financial plan is the big picture. It’s the big map you unfold across the kitchen table. It isn’t just about getting you from here to retirement. It’s about the car repair you need this week, the vacation you want to take next summer, your kids’ activity fees, where you live now, where you would like to live later, the business you would like to start, the help you want to give your aging parents, the education you want to offer your kids. That’s not the sort of trip you leave to chance.

Your financial plan is the big picture. It’s the big map you unfold across the kitchen table. It isn’t just about getting you from here to retirement. It’s about the car repair you need this week, the vacation you want to take next summer, your kids’ activity fees, where you live now, where you would like to live later, the business you would like to start, the help you want to give your aging parents, the education you want to offer your kids. That’s not the sort of trip you leave to chance.

If you are in debt, your financial plan is your route out, even if the road is bumpy. If you have a big goal, your financial plan lays out the action steps, and tracks the progress. A financial plan is exciting and motivating, and it’s one of the most important gifts you can give yourself.

Having that big financial map gives you confidence, because you know where you want to go and you can see the options for getting there.

Mastering Money is a Mindset

As hard as it can be to accept, debt is not a result of not having enough money, it’s the result of spending more than you have. And if you want to change that, it comes down to your mindset.

Here again, are the new money beliefs that can positively impact your finances starting today:

- Financial freedom and peace of mind are possible when consumer debt is eliminated

- Luxury and convenience are not needs

- Successful people are engaged with their spending and saving

- Financially successful people have priorities and are willing to make trade-offs

- A financial plan is a roadmap, not a rule book

By making those beliefs your own, you can stop struggling and start making the most of your money. Getting ahead, starts in your head.

We hope this article has been helpful and provided some practical advice on how you can improve your financial well-being. If you need additional support, please contact one of our Money Coaches today.

Our household has an income of roughly $93,000 per year, but no debt. We’re both retired, so we could not afford to be in debt for long. The only significant debt we took on since I retired (we paid off our mortgage seven years before I retired) was three years ago, to pay for a bathroom renovation, but it was done only to relieve a “cash crunch” situation. We paid for the renovation partly in cash, but mostly through two unsecured lines of credit, and paid them off in full with total interest expense of just over $100. When managed properly, short-term debt can be very useful and will not threaten one’s financial stability. But, if one mismanages it…then one could be very sorry. One of the keys to a happy retirement is having no debt to start off and to make use of lines of credit only when necessary.

Just a quick note from a security perspective. If you use Mint.com and provide your banking details (which is required to automatically track transactions and such) it actually invalidates any liability protections against digital fraud provided by your bank. This is because you’ve willingly provided your password to a 3rd party, which is then used by Mint.com to log into your banking website on your behalf.

This MoneySense article from 2011 on the matter is equally valid today:

http://www.moneysense.ca/magazine-archive/april-2011/hidden-danger-at-mint-com/

Hi Steve,

Congratulations on being debt free. You obviously see that the key to managing short-term debt well, is emphasizing the “short” part of the equation!

It’s imperative when people take on debt, they have a clear plan for paying it back and know how much the debt is going to cost them. If you can say “I’m going to pay $X per month over X number of months and it’s going to cost $X in interest” then you can make an informed decision as to whether this is worth it or not. No doubt the $100 added to your renovation was well worth the expense to have your bathroom renovation done in a timeline that worked for you.

Unfortunately, too many people go into debt without a plan as to how they will pay it back and rather than using their credit for one off “cash crunch” situations, are using it to maintain lifestyles that are unsustainable in the long term. Carrying this debt into retirement can erode a persons retirement funds. If you can’t afford your lifestyle while working, image how tricky it can be to make ends meet when you are on a fixed income and have to pay interest on top of maintaining your lifestyle!

A Spending and Savings Plan can help to ensure that debt is eliminated before retirement. A Money Coach works with clients to build a plan to pay off debt, live within their means and anticipate future expenses so that they don’t end up on the Credit Card or Line of Credit. Having a clear picture of your cash flow, both while working and in retirement is key to having peace of mind.

Enjoy your retirement :-)

-Christine